Financial independence (FI) and early retirement (ER) have become buzzwords in personal finance circles, particularly within the FIRE (Financial Independence, Retire Early) movement. The idea of leaving behind the traditional 9-to-5 work life earlier than expected is appealing to many. However, the road to FIRE requires disciplined planning, strategic saving, and smart investing.

Achieving financial independence in your 30s, though challenging, is entirely possible with the right mindset, strategy, and consistent effort. In this article, we will outline a clear roadmap to help you navigate the path to financial independence and early retirement, starting from your 30s. Whether you are just beginning or have already started the journey, this guide will provide the necessary steps to help you retire earlier than you ever thought possible.

What is Financial Independence?

Before diving into how to achieve financial independence, it’s essential to understand what it means. Financial independence refers to the state where your assets and investments generate enough passive income to cover your living expenses, making it unnecessary to work for a paycheck. Early retirement takes this a step further, allowing you to stop working altogether and focus on passions, hobbies, or other activities that bring fulfillment.

To achieve financial independence, you need to reduce reliance on earned income and cultivate income streams that require minimal effort to maintain, such as investment dividends, rental income, or income from a side business.

Why Start in Your 30s?

Starting your journey to financial independence in your 30s has significant advantages. The earlier you begin, the more time you have to benefit from the power of compound interest. Saving and investing aggressively in your 30s can provide a strong financial foundation for the future. For example, if you invest early, your money has a longer time horizon to grow and work for you. This can result in an exponentially larger nest egg by the time you reach your 40s or 50s, setting you up for early retirement.

One of the key benefits of starting in your 30s is that you are more likely to have fewer family and personal commitments than later in life, making it easier to maintain a high savings rate and financial discipline. Starting in your 30s allows you to take full advantage of your peak earning years and build wealth faster, rather than waiting until your 40s or 50s when it may be more difficult to achieve your goals.

Key Steps to Achieve Financial Independence in Your 30s

Achieving financial independence is a multi-step process that requires discipline, focus, and consistency. Here’s a breakdown of the essential steps to help you achieve your financial independence in your 30s:

Step 1: Set Clear Financial Goals

The first step towards financial independence is setting clear, actionable goals. This is a crucial phase because it gives you direction and purpose. Your financial goals should include both short-term and long-term objectives. For example, short-term goals might include paying off high-interest debt or saving a specific amount for an emergency fund. Long-term goals could involve accumulating enough savings to replace your monthly income through passive income streams.

To calculate how much money you’ll need for financial independence, you can use the 25x rule (an extension of the 4% rule), which suggests that you should have 25 times your annual living expenses saved before you retire. For instance, if your annual living expenses are $40,000, you would need $1,000,000 to reach financial independence.

Step 2: Create a Budget and Track Your Spending

A comprehensive budget is the foundation of your financial journey. Without a budget, it is nearly impossible to know where your money is going and to track your progress. To build wealth and retire early, you need to save a significant portion of your income. The average FIRE adherent saves at least 50% of their income.

Start by tracking your spending and categorizing your expenses into essentials (e.g., housing, utilities) and non-essentials (e.g., dining out, entertainment). Use budgeting tools like YNAB (You Need a Budget), Mint, or Personal Capital to track your income and expenses. This will help identify areas where you can cut back and allocate more towards savings and investments.

Step 3: Build and Maximize Your Income Streams

To retire early, it is not enough to save aggressively. You must also work on building multiple streams of income. Here are some ideas to maximize your income:

- Side Hustles: Side gigs like freelancing, consulting, or even starting an online business can supplement your income and speed up your journey to FIRE.

- Investing: Stock market investing is one of the most effective ways to build wealth. Consider low-cost index funds or ETFs for consistent returns over time.

- Career Growth: Climbing the corporate ladder or gaining additional certifications can significantly boost your earning potential.

The key is to diversify your income streams to ensure that you have multiple sources of revenue, reducing your reliance on a single paycheck.

Step 4: Aggressively Pay Off Debt

Debt is one of the biggest obstacles to financial independence. It is crucial to pay off any high-interest debt, such as credit card debt, as quickly as possible. The longer you carry debt, the more it will erode your ability to save and invest.

There are two primary strategies for paying down debt:

- The Debt Snowball Method: Pay off your smallest debts first, then move to the next largest. This method provides quick wins, motivating you to continue.

- The Debt Avalanche Method: Pay off high-interest debt first, which saves you more money in the long run by reducing interest charges.

Both methods are effective, but the debt avalanche method may be more suitable for those who want to save money on interest over time.

Step 5: Save and Invest Wisely

One of the most critical steps in achieving financial independence is saving and investing wisely. As mentioned earlier, the FIRE movement recommends saving a significant portion of your income—typically 50% or more. This requires cutting back on expenses and prioritizing your future.

In terms of investing, consider the following options:

- Stocks and Bonds: For long-term growth, investing in stocks (particularly low-cost index funds) is crucial. Bonds can offer stability to your portfolio.

- Real Estate: Real estate is another way to build wealth and generate passive income, especially if you invest in rental properties or REITs (Real Estate Investment Trusts).

- Retirement Accounts: Maximize contributions to retirement accounts like 401(k)s and IRAs. Take advantage of employer matches and tax-deferred growth.

The key is to develop a diversified investment portfolio that aligns with your risk tolerance and long-term financial goals.

Step 6: Develop Passive Income Streams

One of the most important components of FIRE is generating passive income. Passive income refers to money earned with minimal effort after the initial setup. Common passive income streams include:

- Dividends from stocks

- Rental income from properties

- Profits from online businesses or digital products

The goal is to create a situation where your passive income covers your living expenses, allowing you to step away from active employment.

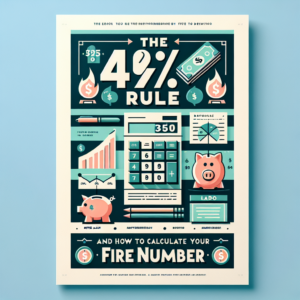

The 4% Rule and How to Calculate Your FIRE Number

The 4% rule is a guideline used by many in the FIRE community. It suggests that you can safely withdraw 4% of your savings each year in retirement without running out of money. To calculate your FIRE number, simply multiply your desired annual expenses by 25. For example, if you need $40,000 per year to live, you would need $1,000,000 ($40,000 x 25) to retire.

By adhering to the 4% rule, you can estimate the amount of savings required to retire early.

Challenges on the Road to Financial Independence

While the road to financial independence can be rewarding, it is not without challenges. Common obstacles include:

- Lifestyle Creep: As income increases, expenses often rise as well. Staying disciplined and not succumbing to lifestyle inflation is key to maintaining your savings rate.

- Unexpected Expenses: Emergencies like medical bills or car repairs can derail your progress. Maintaining an emergency fund is essential.

- Motivation: Staying motivated over a long period is challenging. It’s crucial to remember why you are working towards financial independence and to regularly revisit your goals.

Achieving financial independence in your 30s is an ambitious but attainable goal. By setting clear financial goals, aggressively saving and investing, and creating multiple income streams, you can build a strong foundation for early retirement. While the journey to FIRE requires discipline and sacrifices, the rewards—financial freedom, time, and fulfillment—are worth the effort.

Remember that the earlier you start, the more time you have to build wealth and benefit from the magic of compound interest. So, start today, make intentional financial decisions, and you’ll be well on your way to achieving financial independence and early retirement.

FAQ Section

-

What is the best age to start planning for financial independence? The earlier you start, the better. In your 30s, you have plenty of time to accumulate wealth, but it’s never too late to start.

-

Can you achieve financial independence without a high salary? Yes, financial independence is more about living below your means, saving aggressively, and investing wisely than earning a high salary.

-

How much should you save for retirement in your 30s? Aim to save at least 15% of your gross income, but saving more can help you reach FIRE even faster.

Visit our other website: https://synergypublish.com